Gap Protection

One Small Change, One Large Outcome: Why More Dealers Are Rethinking GAP Chargebacks

GAP chargebacks can quietly reduce dealership profitability. Learn how they work, how no-chargeback GAP differs, and how to evaluate the right GAP strategy.

Most dealerships measure GAP by penetration. How many customers said yes, at what average profit, on what percentage of deals. Those numbers matter, but they describe a single moment at delivery. They say nothing about what happens to that income three, six, or twelve months later when a loan pays off early and the contract cancels.

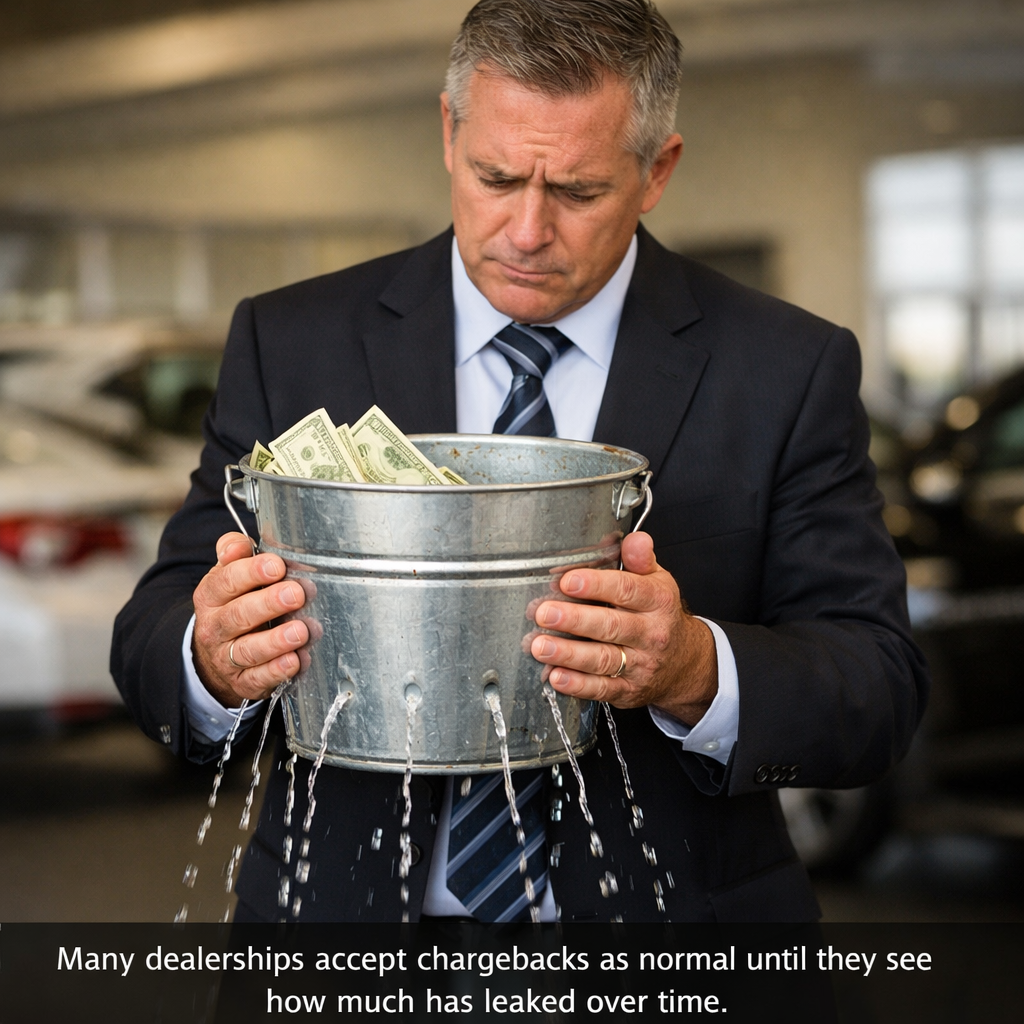

That is where GAP chargebacks live, and it is where a program that looked profitable at the desk can quietly lose money over time. A GAP product can perform well on the menu and still create unexpected financial consequences later. Understanding how chargebacks work is essential to evaluating the true profitability of a GAP program, and it is the reason a growing number of dealers are taking a closer look at how their GAP income is structured. This article explains chargebacks, how traditional and no-chargeback GAP differ, and how to evaluate the right approach for your store.

What Is a GAP Chargeback?

GAP coverage is tied to a loan, so it cancels whenever that loan ends before its scheduled term. When that happens, the unearned portion of the premium is refunded to the customer or lender, and under a traditional program the dealership's commission is reversed on a pro-rata basis. That reversal is the chargeback.

Several common events trigger it. A customer pays off the loan early, refinances with another lender, trades the vehicle in, or the loan ends through repossession or a total loss. Any of these can cancel the GAP contract and create a commission reversal months after the sale was booked. The lifecycle below shows how the same early payoff produces two different outcomes depending on how the program is structured.

- Vehicle Sold

- GAP Purchased

- Loan Paid Off Early

- Cancellation

- Chargeback

- Vehicle Sold

- GAP Purchased

- Loan Paid Off Early

- No Chargeback

Why GAP Chargebacks Matter

Chargebacks matter because they turn income a dealership already recognized into a future liability. That has effects well beyond the single deal. F&I income becomes less predictable, which makes budgeting and performance measurement harder. Accounting grows more complex because reserves have to be tracked and adjustments made as contracts cancel. Cash flow can swing in ways that are difficult to forecast.

There is also a human cost. Finance managers who watch earned commission reverse on deals they closed cleanly months ago can grow frustrated, especially when chargebacks are outside their control. The broader lesson is that a GAP program should be evaluated on net profitability over time, not only on the upfront commission shown at the point of sale. The headline number and the number that actually reaches the bottom line are not always the same.

The Hidden Cost Most Dealers Never Calculate

The most expensive part of chargebacks is the part that never shows up as a single line item. There is the lost commission itself, but there is also the administrative work of processing cancellations, the accounting adjustments, the chargeback reserves that tie up money, and the forecasting challenges that come from unpredictable reversals. None of these are dramatic on their own.

The problem is accumulation. A modest chargeback here and there feels minor, but across hundreds of deals over a year the total can meaningfully reduce dealership profitability without any single moment that makes it obvious. Add the effect on finance manager morale, and the true cost of a chargeback-heavy program is larger than most dealers ever sit down to calculate. Measuring it is the first step toward deciding whether a different structure is worth considering.

How Traditional GAP Programs Work

Traditional GAP exists for a clear and valuable reason. When a financed vehicle is declared a total loss or is stolen, the insurance payout is based on the vehicle's actual cash value, which is often less than the remaining loan balance. GAP covers that deficiency, protecting the customer from owing money on a vehicle they no longer have. It is genuinely useful coverage, particularly for buyers with long loan terms, small down payments, or negative equity rolled into the loan.

Under a traditional structure, the dealership earns income when the product is sold, and that income is subject to cancellation provisions. If the contract cancels before its term, the unearned premium is refunded and the commission is reversed pro-rata. There is nothing wrong with this model, and for many dealers it works well. It simply carries chargeback exposure that has to be understood and planned for rather than ignored. You can see how GAP is positioned for customers on our GAP protection page.

Understanding No-Chargeback GAP Programs

No-chargeback GAP is structured so that the dealership's income is protected when a contract cancels early, depending on the provider's specific terms. The customer protection is the same. What differs is how the dealer's income behaves after the sale. For stores with high early-payoff or refinance activity, that difference can stabilize F&I income and simplify forecasting and accounting.

It is important to be balanced here. No-chargeback GAP is not automatically superior. Providers structure these programs differently, pricing and terms vary, and the protection may apply only under certain conditions or timeframes. A program that eliminates chargebacks but carries higher cost or narrower terms may or may not be the better choice depending on the dealership's situation. The right move is to read the program details carefully rather than assume the label tells the whole story. Our breakdown of no-chargeback GAP goes deeper, and the no-chargeback GAP page covers how it is offered.

| Factor | Traditional GAP | No-Chargeback GAP |

|---|---|---|

| Commission stability | Reversible if the contract cancels early | More stable, depending on program terms |

| Chargeback exposure | Dealer carries pro-rata reversal risk | Reduced or eliminated per the program |

| Cancellation impact | Income returned on early payoff or cancel | Limited income impact, program dependent |

| Forecasting | Less predictable F&I income | Easier to forecast |

| Administration | Reserve tracking and adjustments | Simpler accounting, fewer reversals |

| Dealer considerations | Often lower upfront cost | Pricing and terms vary by provider |

Questions Dealers Should Ask Before Choosing a GAP Provider

The right provider is the one whose program fits how your store actually operates, and the only way to know that is to ask specific questions. Start with the chargeback policy and cancellation terms, since those define your income risk. Then look hard at the claims process and customer experience, because that is what protects your reputation at the moment a customer needs the coverage.

From there, evaluate the administrator's financial strength, the quality of reporting you will receive, the training and support offered to your team, and the overall transparency of the relationship. A provider who answers these questions clearly and in writing is easier to trust than one who relies on a strong rate alone. The goal is to compare programs on net long-term value, not just the commission printed on the rate sheet.

How GAP Fits Into a Complete F&I Strategy

GAP should never be evaluated in isolation. It is one product in a portfolio that also includes vehicle service contracts, Deposit Protect, appearance protection, tire and wheel coverage, and more. Each product has its own value to the customer, its own cancellation behavior, and its own role in the menu. Looking at GAP alongside the rest of the lineup gives a far more accurate picture of F&I performance than studying it alone.

The menu presentation ties the portfolio together. A consistent, transparent process that builds value before price improves penetration across every product, GAP included. For a broader view of building the right lineup, see our guide to the best F&I products for auto dealers. GAP is strongest when it is part of a deliberate strategy rather than a standalone add-on.

Should GAP Be Included in Dealer Reinsurance?

Reinsurance lets dealers participate in the underwriting profit and investment income of the products they sell, and it is one of the most effective long-term wealth tools available. Whether GAP belongs in a dealer's reinsurance position, however, is a genuine question rather than a given. GAP can carry more claims volatility than products like service contracts, and that volatility behaves differently across market conditions.

The answer depends on loss ratios, claims patterns, the dealer's participation strategy, and long-term objectives. Some dealers include GAP and manage the volatility deliberately. Others keep it separate. Neither is automatically correct. This is a decision to model carefully with real numbers, and our dealer reinsurance resources, along with the deeper look at trust accounts and reserve timing, can help frame it.

Training Still Determines GAP Performance

No GAP structure performs on its own. The finance manager presenting it does. Even the strongest product depends on consistent, transparent presentation, and that comes from training. Strong GAP performance starts with discovery and a real needs assessment, so the coverage is tied to the customer's actual loan situation rather than pushed as a generic add-on.

From there it depends on a clear menu presentation, honest communication about what GAP does and does not cover, solid compliance, and the product knowledge to answer questions confidently. Adaptive Training builds those fundamentals, Dynamic Coaching turns them into consistent execution through role-playing and objection handling, and Dealer Timeline keeps the coaching and accountability going over time. A great GAP program with weak presentation underperforms, and a disciplined team gets more from whatever structure they run.

How Elite FI Partners Helps Dealers Evaluate GAP Programs

Elite FI Partners works as an advisor on GAP strategy rather than simply a provider of one product. That means helping dealers compare programs and administrators objectively, evaluating chargeback structures against the store's actual cancellation patterns, and looking at GAP within the full F&I portfolio and menu process instead of in a vacuum. It also means connecting GAP decisions to compliance, training, and, where it fits, dealer reinsurance and long-term profitability.

The aim is a decision the dealer can stand behind for the right reasons. The framework below is the order we think dealers should weigh a GAP program, starting with the customer and ending with the number that actually matters over time.

- Customer Value

- Administrator Quality

- Chargeback Structure

- Training

- Long-Term Profitability

Frequently Asked Questions

What is a GAP chargeback?

A GAP chargeback is a reversal of income a dealership earned on a GAP sale when the contract cancels before its term ends. Under a traditional program, the unearned portion is refunded and the commission is reversed pro-rata when a loan pays off early, refinances, or otherwise cancels.

Why do GAP chargebacks happen?

They happen whenever the financing GAP is tied to ends early. Common triggers include early payoff, refinancing, trade-ins, repossession, and total loss. Because GAP is linked to the loan, anything that closes the loan early can cancel the coverage.

How do chargebacks affect dealership profitability?

Chargebacks turn recognized income into a future liability. They make F&I income less predictable, complicate accounting, require reserves, and can erode net profit over time. A program can look strong on upfront commission and weaker once chargebacks are netted out.

What is no-chargeback GAP?

No-chargeback GAP is structured so the dealership's income is not reversed when a contract cancels early, depending on the provider's terms. The structure and pricing vary by provider, so dealers should review exactly how and when the income is protected.

Is no-chargeback GAP better?

Not universally. It can stabilize income and simplify forecasting, but the tradeoffs, including pricing and terms, differ by provider. Whether it fits depends on a dealership's cancellation patterns, objectives, and overall strategy.

How should dealers compare GAP providers?

Look beyond commission. Compare chargeback policy, cancellation terms, the claims process, customer experience, the administrator's financial strength, reporting, training, support, and transparency. Net long-term profitability matters more than the upfront number.

Can GAP products be included in dealer reinsurance?

Sometimes. GAP can be more volatile than other products, so whether it belongs in a reinsurance position depends on loss ratios, claims volatility, market conditions, and the dealer's participation strategy. It should be evaluated carefully rather than assumed.

How do finance managers reduce cancellations?

Through strong discovery, honest needs-based presentation, clear explanation of coverage and limitations, and proper documentation. Customers who understand and value what they bought are far less likely to cancel.

How does GAP fit into a complete F&I strategy?

GAP is one part of a portfolio that includes vehicle service contracts, appearance protection, tire and wheel, and more. It should be evaluated alongside those products and the menu process, not in isolation.

What should dealerships look for in a GAP administrator?

Financial strength, a clear and fair claims process, consistent approvals, strong reporting, dealer support, training, and transparency. The administrator determines the customer's experience at claim time, which protects the dealership's reputation.

Evaluate GAP Beyond the Commission

The dealerships that get GAP right are the ones that look past penetration and upfront commission to the whole picture: the value to the customer, the quality of the administrator, the chargeback structure, the training behind the presentation, and the net profitability over time. Sometimes that points to a traditional program, and sometimes it points to a no-chargeback structure. The right answer depends on the store.

If you want to evaluate your GAP strategy with that complete view, Elite FI Partners can help you compare programs and administrators, model the chargeback impact, and connect GAP to your training, menu, and reinsurance strategy. Get in touch with our team to review your GAP approach.

By Michael Aufmuth, Agency Principal · Elite FI Partners