Reinsurance

CFC vs NCFC vs DOWC vs Retro: The Ultimate Dealer Reinsurance Comparison Guide

Compare CFC, NCFC, DOWC, Super CFC, and Retro reinsurance structures side by side. A dealer-focused guide to control, risk, tax position, fees, scalability, and which profit participation structure fits your store and growth plan.

Every dollar of F&I profit your store sends to an outside provider is a dollar you could have kept, invested, and grown. Reinsurance and profit participation are how dealers stop renting their underwriting profit and start owning it. The harder question is not whether to participate. It is how, because the structure you choose shapes everything that follows.

The decision between Retro, CFC, Super CFC, NCFC, and DOWC is not an F&I department line item. It is a capital and wealth decision that touches control over your reserves, the underwriting profit you keep, your tax position, how fast reserves compound, your administrative load, your reporting visibility, your risk exposure, and your ability to scale or eventually exit. Pick the structure that fits your production today and your goals five years out, and the program quietly builds a second business inside your dealership. Pick the wrong one, and you either leave money on the table or take on complexity your store is not ready to carry.

This guide compares the major structures in plain language, side by side, so principals, general managers, CFOs, and finance directors can evaluate them against real numbers rather than sales pitches. At Elite FI Partners, we help dealers run that comparison against their actual production, product mix, claims history, reserve goals, and growth plans through our dealer reinsurance programs and a no-cost review of any program already in place.

What Is Dealer Reinsurance?

Dealer reinsurance is the mechanism that lets a dealership participate in the underwriting profit and investment income generated by the F&I products it already sells. Vehicle service contracts, GAP, tire and wheel, appearance protection, key replacement, and similar protection products all carry premium that, in a traditional setup, flows to the administrator and the insurance company. Reinsurance and profit participation redirect a meaningful share of that economic value back to the dealer.

The mechanics are straightforward. When you sell a protection product, part of the price covers expected claims, part covers administration, and part is underwriting profit plus the investment return earned on reserves while claims pay out over the life of the contract. Reinsurance puts the dealer on the receiving end of that profit and investment income instead of leaving it with a third party. If you want the full primer before going deeper, our explainer on what dealer reinsurance is walks through it step by step.

The practical payoff is that reinsurance moves the dealer beyond front-end commission. Commission is earned once and gone. A well-run reinsurance position keeps earning for years as contracts mature, claims stay below premium, and reserves compound. That is the difference between income and wealth, and it is why successful dealer groups treat their reinsurance company as a core asset rather than an F&I afterthought.

Why the Reinsurance Structure Matters

All of these structures share the same goal of returning underwriting profit to the dealer. Where they diverge is in the terms of that ownership, and those differences decide whether a program fits your store. Before comparing names, know which variables actually move the needle.

Control over investments, claims handling, and reserves, which ranges from very little to nearly total.

Capital requirements, since some structures need real capitalization and ongoing funding while others ask almost nothing up front.

Tax treatment, because certain structures may qualify for elections that change how premium and investment income are taxed. Those outcomes depend on your facts and qualified tax counsel.

Premium caps that limit how much premium can flow through each year, which directly limits scalability.

Administrative complexity across entity formation, accounting, audits, and compliance.

Risk exposure, because owning more of the profit also means owning more of the claims risk.

Investment flexibility, meaning who decides how reserves are invested and how much upside the dealer captures.

Reporting transparency into net premium, claims, fees, and reserve balances.

Scalability, or whether the structure still fits when your volume doubles.

Exit strategy, covering how easily reserves can be accessed or value transferred when you sell the store.

Dealer size and production volume, since the right answer for one rooftop is rarely the right answer for a 12-store group.

Weighing these honestly is the entire exercise. Our team uses a structured dealer reinsurance comparison tool to model how each option performs against your numbers, and you can also compare dealer reinsurance structures side by side on our site.

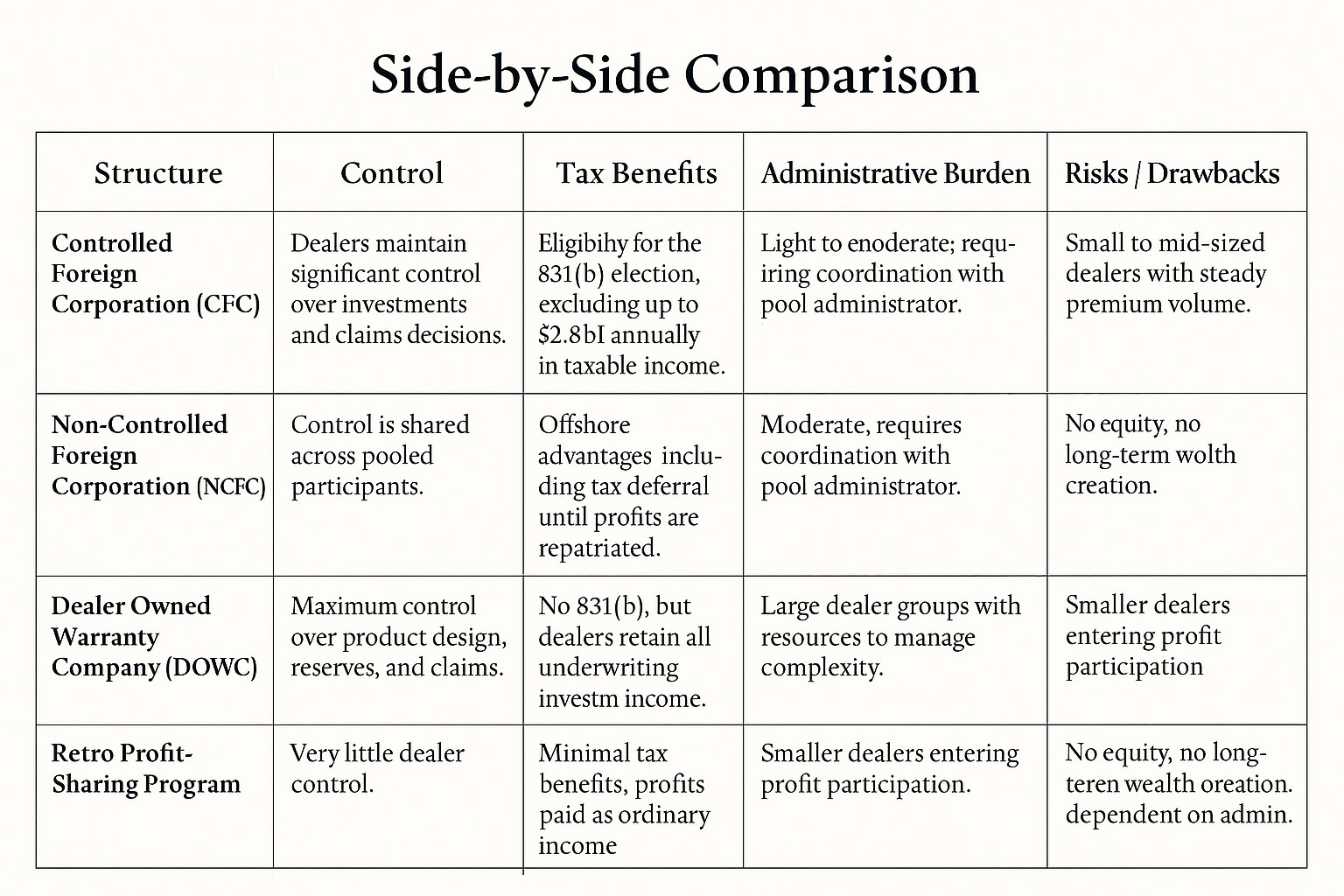

Quick Comparison: CFC vs NCFC vs DOWC vs Retro

The table below summarizes how the five structures compare across the factors dealers ask about most. Treat it as a map, not a verdict. The right fit depends on your production and goals, which the sections that follow address in detail.

| Factor | Retro | CFC | Super CFC | NCFC | DOWC |

|---|---|---|---|---|---|

| Ownership | None (profit share) | Dealer-owned | Dealer-owned | Shared / pooled | Dealer-owned |

| Control | Low | High | High | Moderate | Highest |

| Setup complexity | Minimal | Moderate | Moderate | Low–moderate | High |

| Premium limits | None | Capped (831(b)) | No cap | Program dependent | None |

| Tax advantages | Limited | Possible* | Possible* | Possible* | Possible* |

| Cash flow timing | Periodic payout | Builds in reserve | Builds in reserve | Builds in pool | Dealer controlled |

| Risk level | Low | Moderate | Moderate–higher | Shared | Highest |

| Scalability | Low | Moderate | High | Moderate–high | High |

| Admin load | Very low | Annual filings | Annual filings | Lower per dealer | Substantial |

| Best fit | Entry / lower volume | Steady producers | Growing volume | Scale, less burden | Large groups |

*Potential tax treatment depends on your facts and the guidance of qualified tax counsel. Nothing here is tax advice.

Retro Profit Participation

A retro, short for retrospective commission or profit-sharing arrangement, is the simplest way for a dealer to share in underwriting results without forming a company. The administrator tracks the performance of the dealer's book and pays back a share of the profit at set intervals, typically annually, once claims and expenses are accounted for. It is the natural on-ramp, letting a store see real profit participation dollars and learn how product performance drives results before committing to entity formation.

Benefits: low barrier to entry with little or no startup cost, no new entity to form or maintain, a simple structure that is easy to explain to ownership, and a practical starting point for dealers new to profit participation.

Limitations: less control, since the dealer does not own the reserves or direct the investments; less transparency into how profit is calculated; little or no investment strategy, so the dealer misses the compounding upside; and lower long-term wealth potential than dealer-owned structures.

Best fit: lower-volume stores, dealers testing reinsurance for the first time, and dealers not yet ready to form and run their own company. Many graduate into a dealer-owned structure as volume grows. Read more on the retro profit participation page.

CFC Reinsurance

A Controlled Foreign Corporation, or CFC, is the most common dealer-owned reinsurance structure. The dealer establishes and owns a reinsurance company that assumes risk on the products sold at the store. Premium flows into the dealer's company, claims are paid from it, and the underwriting profit plus investment income accrues to the dealer rather than a third party. The CFC is where most dealers first experience true ownership.

Many CFCs are set up to make the IRS 831(b) election, which can change how a qualifying amount of net premium is treated for tax purposes, subject to current IRS limits and the guidance of your own tax advisor. We do not make tax promises, and neither should anyone selling you a structure. The right move is to model it with qualified counsel.

Benefits: a genuinely dealer-owned structure with the dealer as principal; strong profit participation capturing underwriting profit and investment income; potential tax advantages where the dealer qualifies and elects appropriately; far more control than a retro over claims, reserves, and investments; and a proven long-term wealth-building tool for steady producers.

Limitations: premium caps tied to the 831(b) election can limit annual volume; setup and annual administration, including accounting and compliance, are real obligations; and proper tax and legal guidance is required to set up and maintain it correctly.

Best fit: dealers with consistent F&I production who want ownership, control, and long-term wealth building without the heavier demands of running a full warranty company. Explore the details of our CFC reinsurance program to see whether your volume supports it.

Super CFC Reinsurance

The Super CFC was designed to solve the single biggest constraint of a traditional CFC: the premium cap. As a store grows, the 831(b) election that makes a small CFC attractive can become the very thing that holds it back. The Super CFC keeps the dealer-owned, dealer-controlled benefits while removing that ceiling, which often makes it the structure that finally matches the size of the opportunity.

No premium cap positioning, so the structure accommodates volume that would overflow a capped CFC and growth does not force a restructure.

Scalability for higher-volume dealers, designed to grow with stores writing meaningful monthly contract counts and adding rooftops.

Retail cost accounting advantages where applicable, which may improve how reserves and profit are recognized depending on how the program is structured. Confirm the specifics with your advisors.

A stronger fit for larger or growing groups, usually the next logical step when a CFC starts to feel small but a full DOWC is not yet warranted.

Best fit: higher-volume single stores and dealer groups that have outgrown, or expect to outgrow, a capped CFC but are not ready for the full administrative weight of a DOWC. See the full breakdown on our Super CFC reinsurance page.

NCFC Reinsurance

A Non-Controlled Foreign Corporation, or NCFC, lets a dealer participate in offshore reinsurance economics without holding the same individual control as a CFC or DOWC. Rather than the dealer being the controlling owner, participation is structured so that no single dealer controls the company, often within a pooled arrangement that spreads results across multiple participants. For the right dealer, the NCFC trades a degree of control for simplicity and a lighter operational footprint.

Benefits: access to offshore reinsurance benefits without the full control burden of a CFC, a pooled structure that can stabilize results across a larger book, lower operational complexity for the individual dealer, and potential tax benefits depending on the structure and your advisor's guidance.

Limitations: less direct control over investments and claims than a dealer-owned company, more dependence on how the overall program is structured and managed, and a poorer fit for dealers whose primary goal is maximum ownership.

Best fit: dealers who want reinsurance participation with less administrative burden and are comfortable trading some control for simplicity. Learn more about NCFC reinsurance and how it compares.

DOWC Reinsurance

A Dealer-Owned Warranty Company, or DOWC, is the most control-rich structure available to dealers. It is a domestic company, owned by the dealer, that operates as a warranty company in its own right. Rather than only reinsuring risk, a DOWC can issue contracts, design products, manage reserves, and capture both underwriting profit and investment income at the highest level of ownership. It is the enterprise-grade option, offering the most upside and flexibility and asking the most in return.

Strengths: a domestic structure many dealers prefer over offshore arrangements, outright ownership of the warranty company, the highest degree of control over products, reserves, claims, and investments, the ability to issue contracts and shape product design directly, and strong profit potential plus branding advantages for groups that want their own warranty identity.

Limitations: more complexity across formation, accounting, and ongoing operations; more compliance responsibility that the dealer ultimately owns; and higher administrative expectations that require capable partners or internal infrastructure.

Best fit: larger dealers, dealer groups, and dealers who want maximum control and a long-term, enterprise-level structure they can build a brand and a balance sheet around. Our DOWC reinsurance page covers how these companies are built and run.

Which Reinsurance Structure Is Best for Your Dealership?

There is no universal answer, and any partner who gives you one before looking at your numbers is selling, not advising. The right structure is the one that matches your current production and your future plans. The factors that decide it are specific to your store.

Monthly VSC volume, the engine of most reinsurance programs and a primary driver of which structure makes sense.

Total product production, since the full mix of protection products, not just VSC, determines how much premium is available to capture.

Claims performance, because loss ratios shape both the profit you keep and the risk you can comfortably own.

Product mix, as stable products behave very differently from volatile ones inside a reinsurance company.

Growth goals, so a store adding rooftops does not lock into a structure it will outgrow in two years.

Ownership structure, since single owners, partners, and family groups have different priorities for control and succession.

Tax strategy, which the structure should complement, decided with your advisors.

Appetite for control, because some dealers want to run the company and others want the upside with less involvement.

Need for cash flow, weighing near-term access to dollars against long-term reserve growth.

Long-term exit planning, since how the reserves and company factor into an eventual sale matters more than most dealers expect.

The honest path is to model two or three structures against these inputs and compare the outcomes side by side.

Common Mistakes Dealers Make When Comparing Reinsurance Programs

The same avoidable errors show up again and again when dealers evaluate programs.

Comparing only the headline commission. The biggest advertised number is rarely the most profitable deal once fees and net premium are accounted for.

Ignoring fees. Administration, ceding, and other charges quietly erode results. Understanding the full dealer reinsurance costs and fees picture is essential.

Not reviewing claims trends. A program looks great until a rising loss ratio eats the profit. Claims history is a leading indicator.

Not understanding premium caps. Locking into a capped structure right before a growth phase forces an expensive restructure later.

Not knowing who controls investments. Investment income is a major part of long-term returns, so you should at least know who directs it.

Not reviewing reporting transparency. If you cannot see net premium, claims, and reserves clearly, you cannot manage the asset.

Choosing a structure based on another dealer's store. Your neighbor's DOWC may be perfect for them and wrong for you. Volume, mix, and goals differ.

Not aligning reinsurance with F&I training and product performance. The structure cannot fix weak product penetration. The two have to move together.

For a deeper, owner-level checklist, our dealer reinsurance audit checklist walks through how to review fees, claims, and net premium the way an owner should.

Why Reinsurance Alone Is Not Enough

A reinsurance structure is a container. What you put into it is what matters. The most elegant CFC or DOWC produces little if the store is not selling enough product, structuring deals well, and keeping claims in check. Structure and production have to advance together.

A dealer with strong product penetration, a disciplined menu process, and a well-trained finance team will outperform a higher-volume store with a fancier structure but weak fundamentals. The reserves only grow if the products are sold consistently and the deals are clean.

That is why Elite FI Partners treats reinsurance as one part of a complete F&I operating system rather than a standalone product. The same engagement that helps you choose a structure also strengthens the production that feeds it through our F&I products for dealerships, adaptive finance training, a proven menu process, hands-on dealer support, virtual F&I capabilities, fixed ops automation, and reporting and performance management that keep the whole system accountable. Reinsurance works best when product mix, deal structure, training, and compliance reinforce one another.

That product depth spans every channel a dealer might run, including automotive F&I products, vehicle service contract programs, RV F&I products, powersports F&I products, marine F&I products, commercial and fleet F&I products, appearance protection programs, and GPS tracking solutions. The broader and more stable the production, the more there is to capture inside whatever structure you choose.

How Elite FI Partners Helps Dealers Compare CFC, NCFC, DOWC, Super CFC, and Retro

Choosing among these structures should feel like a guided analysis, not a leap of faith. Our role is to put your numbers, not a brochure, at the center of the decision.

Evaluate your current program and whether it still fits if you already participate.

Compare structures side by side, modeling Retro, CFC, Super CFC, NCFC, and DOWC against your real production.

Review fees and transparency so nothing hides in the statement.

Analyze your product mix to identify which products belong in a reinsurance position and which do not.

Model production based on your volume, claims, and growth assumptions.

Identify missed profit opportunities, where gaps in penetration often represent the fastest gains.

Build a stronger F&I process by tightening the menu, training, and deal structure that feed the program.

Support implementation with trusted administrators and advisors.

Train the finance team so production stays consistent and compliant.

Monitor ongoing performance so the structure keeps fitting as the store evolves.

Timing matters too. If you are weighing when to make a move, our perspective on when the right time is to leverage reinsurance and our broader overview of dealer reinsurance and profit sharing programs are good companions to this guide.

Frequently Asked Questions

What is the difference between CFC and NCFC reinsurance?

A CFC is a dealer-owned, dealer-controlled reinsurance company, often set up with the 831(b) election, giving the dealer direct say over investments and claims along with strong profit participation. An NCFC is structured so that no single dealer controls the company, frequently within a pooled arrangement. The NCFC trades individual control for lower complexity, while the CFC prioritizes ownership and control.

Is a DOWC better than a CFC?

Neither is universally better. A DOWC offers the most control and ownership, including the ability to issue contracts and design products, but carries substantial administrative and compliance responsibility. A CFC delivers genuine ownership and profit participation with a lighter operational load. Larger groups that want maximum control often choose a DOWC, while steady producers frequently find a CFC or Super CFC fits better.

What is retro profit participation?

A retro is a profit-sharing arrangement in which the administrator pays the dealer back a share of underwriting profit at set intervals, usually annually, without the dealer forming a company. It is the simplest way to participate, with a low barrier to entry, but it offers less control, less transparency, and lower long-term wealth potential than dealer-owned structures.

When should a dealership move from retro to reinsurance?

The usual trigger is consistent F&I production that can support the reserves and administration of an owned structure. When a store is writing steady volume and wants control, investment upside, and long-term wealth rather than periodic payouts, moving from a retro into a CFC or Super CFC is typically the next step. Model the decision against actual volume and claims, not a rule of thumb.

What is a Super CFC?

A Super CFC is a dealer-owned reinsurance structure designed to remove the premium cap that limits a traditional 831(b) CFC. It keeps the ownership and control benefits of a CFC while accommodating higher premium volume, which makes it well suited to growing stores and dealer groups that have outgrown, or expect to outgrow, a capped structure.

Which dealer reinsurance structure gives the most control?

A DOWC gives the most control. As a dealer-owned domestic warranty company, it lets the dealer issue contracts, design products, manage reserves, and direct investments at the highest level. That control comes with the most administrative and compliance responsibility, so it fits dealers and groups ready to operate at an enterprise level.

How do fees impact dealer reinsurance performance?

Fees can be the difference between a strong program and a mediocre one. Administration, ceding, and other charges reduce net premium and compound over time, so a program with an attractive headline number can underperform a leaner one. Reviewing the full fee picture and reporting transparency is essential before committing to any structure.

How does Elite FI Partners help dealers choose the right structure?

We model Retro, CFC, Super CFC, NCFC, and DOWC against your actual production, claims, product mix, and growth goals, review the fees and transparency of any current program, and identify missed profit opportunities. We then support implementation with trusted administrators, train the finance team, and monitor performance so the structure keeps fitting as your store grows.

Final Thoughts

Choosing between Retro, CFC, Super CFC, NCFC, and DOWC is one of the most consequential financial decisions a dealer will make. The best structure is not the one with the loudest pitch or the one your neighbor uses. It is the one that fits your current production and long-term goals, with control, risk, tax position, and scalability all weighed against your real numbers.

Get the structure right and reinsurance becomes a durable second business inside your dealership, compounding profit from products you already sell. Get the supporting production, process, and reporting right alongside it, and that business keeps growing for years.

If you want clarity on which structure fits your store, contact Elite FI Partners. We will review your current program, break down the fees, model your production, and help you decide whether Retro, CFC, Super CFC, NCFC, or DOWC is the right fit. Call 520-631-0465 or explore our dealer reinsurance programs to start the conversation.

By Michael Aufmuth, Agency Principal · Elite FI Partners